The German expat insurance market be like: “click here for some insurance – good luck and goodbye.”

—Max

The insurance broker owes his client the selection and maintenance of the best possible insurance cover.

—IHK, translated from German

When I moved to Germany, I wished I had someone to guide me through this German insurance jungle – in my language.

—Max

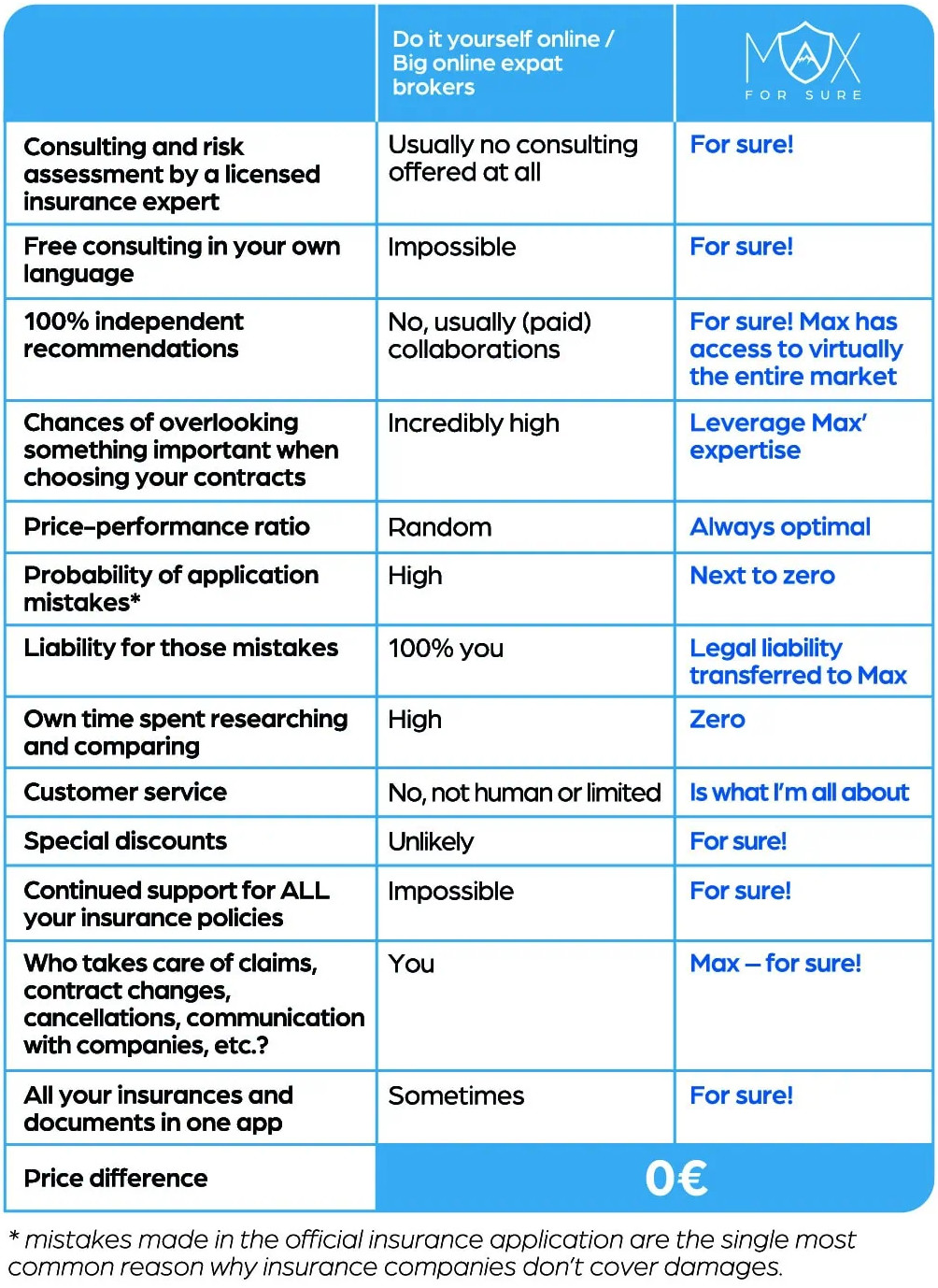

Get expert advice from a licensed and fully independent broker who literally speaks your language.

With Max as your insurance guide, you’re never alone in navigating the complexities of insurance. Whether you have questions, need assistance with claims, or want to adjust your policies, I’m here for you every step of the way – and at no extra cost to you.

Moreover, no matter the circumstance, your insurance details are conveniently at your fingertips. With my sleek, complimentary app, you’ll always have a tidy overview of your contracts and easy access to essential documents whenever you need them.

Unlike many in the industry, I operate as a fully independent insurance broker. I don’t represent specific companies; instead, I offer access to virtually all products on the market. This unbiased approach guarantees that your insurance solution is tailored precisely to your requirements.

IHK, translated from German

The broker is the fiduciary trustee of the customer and as such is obliged to safeguard the interests of the policyholder in the best possible way. He is independent of insurance companies.

At no extra cost whatsoever, max for sure offers expats the unique possibility to get professional insurance advice in their own language. This way, Max’ expertise can be leveraged in order to

Insurance brokers are insurance mediators who legally stand on the side of the customer. It’s their task to inform clients about possibly overlooked financial risks, to provide professional consultation when needed and to tailor an insurance solution which is based on a client’s actual (documented) needs and wishes. Similar to lawyers or tax consultants, they can only become active for their clients after having been given an explicit mandate. Insurance brokers are independant – as opposed to insurance representatives who work for one or multiple insurance companies – and are legally required to serve in their clients’ best interest. Most importantly, insurance brokers actually carry full legal liability for their consultations, recommendations and solutions they mediate.

The broker’s job doesn’t end after an insurance solution has been provided. He or she remains at the client’s disposal for questions, assistance and necessary future contract adaptations. As such, he or she acts as a portfolio manager taking care of all of his clients’ insurance needs.

The insurance broker is usually not paid directly by the client but rather by insurance companies after mediating a certain contract. The broker’s legal liability to act in the client’s best interest ensures that the mediated products don’t exceed actual needs and wishes. The client does NOT pay a higher fee compared to getting the contract directly with the insurance company or via online comparison portals. This remuneration method ensures that the client is under no time constraint when it comes to finding and preparing the right solution.

Becoming an insurance broker in Germany requires passing a theoretical exam based on a three-year curriculum as well as a practical exam in front of a jury. On top of that, the broker is a mandatory member of a German Chamber of Commerce (IHK), who issues the registration number and acts as a control body. All aspiring brokers are subject to a thorough European-wide background check involving their finances and criminal records among others.

The German insurance market is highly complex. To ensure top-quality consulting services in insurance, I focus solely on insurance consulting and do not engage in investment consulting. Instead, I collaborate with a highly experienced investment specialist who will handle all your investment-related needs. This partnership guarantees you the best expertise and service in both insurance and investment domains.

First and foremost in getting your overall insurance set-up in line with your actual needs and preferences. To accomplish this, clients can count on free-of-cost consultations introducing them to the possibilities and limitations of the German system as well as an assessment of their current set-up.

Next to that, I provide on-demand insurance consultations and solutions focussing primarily on all sorts of private insurances such as Berufsunfähigkeitsversicherungen (occupational disability insurance), private health insurance, pension insurance, private liability insurance, etc.

If you seek guidance and consultation on all your insurance needs in Germany, wish to evaluate the price-performance of your current portfolio, or require expert recommendations for a specific insurance, you’ve landed in the right spot.

Simply fill in the contact form to specify your needs and to set up a free consultation with Max.

Yes, absolutely!

With average pensions in Germany currently already cutting most pre-pension salaries more than in half, preventing old-age poverty is a topic of such incredibly high social relevance that still hasn’t fully reached the general populace.

The German Federal Pension Insurance Scheme itself has meanwhile issued a warning that citizens can only count on the pension system so far as it provides additional funds for retirement, adding that the main source of retirement income is to be secured through private contracts such as pension insurance.

Raising awareness about this pressing issue and helping to prevent old-age poverty by getting people the right pension contract thus is one of my key assignments.

None. In order to warrant an all-inclusive service and to avoid any time constraints, there are no monthly or annual fees nor is there an hourly consultation compensation. I get paid directly by insurance companies for mediating their products. This commission is already included in the insurance premium. This is because the commission is part of the insurance product’s price make-up. There should thus not be a considerable (or any) price difference between a contract mediated by me and one contracted online or via other brokers or representatives.

Only for certain pension products which are by themselves commission-free, I charge a consultation fee and/or an ongoing remuneration. If that is the case, this remuneration agreement is explicitly communicated and regulated via a separate fee agreement.

For three reasons: personal values, legal liability and reputation.

While every field may have its share of unscrupulous individuals, my commitment is to provide clients with the level of service I would expect for myself. This was my motivation for entering the brokerage profession in the first place.

Furthermore, by utilising my services, clients transfer legal liability to me. This means I’m accountable for any errors or actions not aligned with their best interests, potentially in a court of law.

Moreover, in today’s digital era, transparency reigns supreme. Reviews and reputations are vital, and unethical practices are likely to surface, jeopardising any business’s future. In essence, ethical conduct isn’t just a moral imperative; it’s also a pragmatic approach in maintaining a sustainable business in the long run.

I don’t offer any products that don’t pass my strict quality requirements. Other than that, I offer almost the full bandwidth of private and business insurances on the market. As one can impossibly be an expert in everything though, I have decided to transfer bAV and bKV requests to other independent brokers who specialise specifically in these products.

I offer consulting and insurance solutions for people who are self-employed as well as “freiberuflich”: Betriebshaftpflicht, Berufshaftpflicht, Vermögensschadenhaftpflicht, Rechtsschutz, Sach-Inhalts, etc,

It barely gets any more independent than this. As an insurance broker, I am mandated by law to function as an impartial intermediary. I do not hold shares in any specific companies that could potentially compromise my independence. Moreover, unlike the majority of brokers or representatives, I operate entirely free from any sales quotas.

What’s more, I do not, in any way, engage in any kind of network marketing activities, I do not have or look for (sales) partners, do not plan on doing so in the future and wish to clearly distantiate myself from these kind of activities. Max for sure is about me, Max, offering his clients the best possible insurance consulting, coverage and service.